We help organisations and their owners and directors.

The organisations are UK based as well as international groups looking to invest into the UK. They tend to be established and growing entities.

We love working with clients across a broad range of sectors but have particular expertise in the areas listed. We also work with private individuals and families with their own personal tax matters, whether their wealth is UK-based or international.

Goodman Jones are not just Chartered Accountants and Auditors – but advisers who are passionate about providing an outstanding tailored service to each of our clients.

Our range of services are our response to listening to what our clients value.

We are not just Chartered Accountants and Auditors – but business advisers who are passionate about providing an outstanding tailored service to each of our clients.

Matt is experienced in helping companies that are looking to grow. Specifically, he has been working with a number of companies assisting with the development of their management accounting and reporting for internal management control and also banks and external funders. In particular, Matt has worked with a number of property and construction clients where his detailed understanding of project accounting has added significant value.

It is with deep sadness that we announce the passing of Larry Phillips, a former Managing Partner of Goodman Jones, on Tuesday 5th August.

Larry spent his entire career working at Goodman Jones, starting as a trainee and rising to Managing Partner, a position he held for an unprecedented 15 years. He brought so much energy and passion to the firm and so many of the brilliant things the firm has done can be directly traced back to Larry. He was also right at the beginning of the introduction of IT to the accounting profession and his foresight helped lead to the creation of the highly successful IT business, Fitzrovia IT.

Matt Cook, Managing Partner of Goodman Jones, said:

“Larry was an incredible colleague, friend and mentor to many at GJ as well as all his clients. He will be remembered for his mantra of ‘It’s all about relationships’, something he brought to every part of his life. He was very proud of what he built at Goodman Jones, a firm that has great people who work hard to provide an outstanding service to our clients and enjoy coming to work each day. He will be sorely missed by us all. Despite his retirement just over a year ago, he loved keeping in touch and providing us with his valuable advice in his unique friendly manner whenever needed. His legacy at Goodman Jones will remain for many years – largely due to the structure of the firm put in place by Larry that has made Goodman Jones a successful firm and has allowed us to remain independent despite all the external investment currently being seen in similar firms.

Our thoughts are with the family he loved so very much at this very sad time. He will be deeply missed but his legacy will not be forgotten”

Thank you Larry.

.

0

Comment on this...

Share

Goodman Jones remains committed to being an independent firm. We will continue to prioritise a service that is truly valued by our clients. To achieve this, we invest significantly in our people, allowing them to flourish and contribute their own energy and ideas for the benefit of everyone we work with

We are delighted to announce that Matt Cook has been elected to become the firm’s next Managing Partner with effect from 1st June.

Matt has been with the firm since 2000 when he joined as a trainee in the audit and accounts team. Since then, Matt has held several high-profile positions in the firm including IT partner since 2015 and more recently, Finance partner since 2022.

“It’s such an exciting time to be in the profession and I am honoured to be leading the firm in this next stage of our development. Focusing on long term goals has always been key to our success, so I am aware of the responsibility of guiding a 90 year-old business on the next steps, building on the strong foundations that have been set by others before me”.

“Despite the significant changes our market is facing with AI advancements and investment from Private Equity firms changing the shape of many players, Goodman Jones remains committed to being an independent firm. We will continue to prioritise a service that is truly valued by our clients. To achieve this, we invest significantly in our people, allowing them to flourish and contribute their own energy and ideas for the benefit of everyone we work with.”

Matt will continue to work with his client base while holding this role.

As we welcome Matt, we also say thank you to Julian Flitter who steps down at the end of his term in the role. Under his leadership, the firm accomplished several notable achievements. These triumphs include the introduction of new EDI policies such as flexible working and the celebration of cultural events. The firm also picked up the London Mayor’s Business Climate Challenge award in recognition of work done on sustainability.

Julian also oversaw the recent move to our new Fitzrovia office which supports both inclusivity and sustainability with a flexible working environment, as well as having a BREEAM Excellent rating for its top-tier energy efficiency and minimal environmental impact.

The firm is well positioned, and we look forward to the future.

0

The information in this article was correct at the date it was first published.

However it is of a generic nature and cannot constitute advice. Specific advice should be sought before any action taken.

If you would like to discuss how this applies to you, we would be delighted to talk to you. Please make contact with the author on the details shown below.

Comment on this...

Share

We sat down with Joe McGurk from Kene Partners to discuss the latest developments in R&D; the winners and losers from the Autumn Statement and what's behind the recent rise in HMRC inquiries.

On Tuesday 29th November we sat down to discuss the latest developments in R&D; the winners and losers following the Autumn Statement and the recent rise in inquiries. Joining Goodman Jones Partner Matt Cook was Joe McGurk, Managing Director at Kene Partners.

Transcript

Matt: 0:01 Good morning and welcome. I’m Matt Cook, Partner here at Goodman Jones. I’m joined today by Joe McGurk. He is Managing Director of Kene Partners. Kene Partners are a specialist research and development tax advisory firm, who we’ve worked closely with over the last few years and today I’m going to have a brief discussion around the latest developments in the world of R&D. So morning, Joe.

Joe: 0:23 Pleasure to be here.

Matt: 0:24 Good to chat to you again and I think the best place to start is the Autumn Statement, announced a few days ago. R&D was specifically mentioned in what he said might be announced. So, it’s positive that it’s high on the agenda. However, not all was good news. So would you mind giving an overview of what was announced?

Joe: 0:47 Yeah, certainly. I mean, I think there was some trepidation in the industry, they have received a lot of bad press. And some of we’ll come to later. Earlier in the week and the build up and Jeremy Hunt has quite a history of making quite radical changes when needed. So, we were quite nervous. Positive, as you say that that R&D still remains high on the agenda, which is essential for UK PLC and he recognizes that.

The negative being that I suppose, an opportunity to reduce the damage that’s done by some of the erroneous claiming that purported to have been happening, he did slash the rates of benefits. So super deduction is down from 130% to 86%. The tax credit itself, which was previously around at 14.5% is now 10%. But then on the other side, RDEC was increased as a credit from 13% to 20%. So, he took with one hand and gave the other.

Joe: 1:49 So, SMEs will see a real terms deduction, loss making SMEs will see a real time deduction from around about 33% to 19%. Profit making SMEs will go from a proper above a certain level to £250,000 will go from around 25% to 22% because it dovetails with the increase in corporation tax, that’s coming in on the first of April. And then more damagingly, those lower profit making SMEs will see their credit reduced from between 18% down to around about 8%.

Matt: 2:26 Large companies, you mentioned the RDEC is for large companies…

Joe: 2:30 Yes.

Matt: 2:30 A large company is?

Joe: 2:32 An RDEC company? over 500 employees, over 100 million in turnover, over 86000 euros in assets, they will actually see a 50% increase in cash receipt from their expenditure. So, up from a real term credit of 10% to 15%.

Matt: 2:53 So closing the gap, but indeed a big hit for most claims, which is SMEs.

Joe: 2:59 Predominantly, the claims made in the UK are by SMEs. Now, the largest amount of benefits typically goes to RDEC firms. And I think we can recognize that its FTSE companies and the larger PLCs that are based in the UK are doing some really legitimate R&D. It’s great that they’re encouraged and rewarded. Unfortunately, the purpose of the incentive is to reward innovation at all levels. And I’m not sure it quite encourages innovation at the same level it did previously.

Matt: 3:28 And how do you think this has gone down with the SMEs? I heard you saying there’s been quite a backlash…

Joe: 3:36 I mean, various trade bodies and industry bodies are compiling a list of complaints, not just the R&D advisory sector. That’s across big four accountancy firms, various other larger SME firms. There’s also trade bodies because this incentive is so valuable, it provides so much of the working capital that businesses need in their early years and to encourage that further development of products and processes, new systems and sciences, that without it, frankly, the coughers are going to run dry pretty quickly.

People forecasting cash flow for the next two or three years are starting to look around for external investment. There’s a lot of talk already about jobs moving overseas, which is quite alarming. I think Jeremy is going to have to address that problem at some point.

Matt: 4:25 Do you think he’ll change it?

Joe: 4:27 Well, I suppose I hope that he will. There’s actually some suggestion that he might look at the impact on the SME environment in the UK and maybe recognize that it’s going to negatively impact those businesses. As such, he might retract a little bit of the restriction before they come to a final decision about the future of the R&D incentive scheme.

Matt: 4:56 I mean, you mentioned previously, in the run up to the autumn statement, there was a number of articles appeared in the press, talking about R&D, how there was a high number of bogus claims, and even some concerning reports of abuse and fraud. I just wonder what your thoughts are on this and do you think this is why the chancellor has reduced the level of support particularly for SMEs?

Joe: 5:21 Yeah, I mean, there are a number of things to cover here. The first is let’s talk about outright fraud, it’s undeniable that fraud has been taking part in the scheme. There was a house of laws subcommittee on Monday before the Autumn Statement, which was attended by representatives from the R&D industry, and they address questions of fraud in that meeting, with varying levels of success, but the well-publicized prosecutions of fraudsters, I think there was another case recently in which eight people have been prosecuted. One of them is in fact a tax advisor for submitting 100 claims, erroneous claims totalling value or loss to the exchequer of 16 million pounds. So, that’s 160,000 pound claims. Bear in mind, the average is between for an SME is between 50,000 and 60,000 pounds. It’s not just greedy, it’s blatant, and frankly, it screams of people who are becoming quite reckless in their attempts to defraud HMRC.

Now, that’s the most damaging case, there are also those people who are submitting claims erroneously. So that comes down to a couple of things. One is their understanding, as taxpayers, as businesses, as advisors of R&D and what qualifies. And they may very honestly be submitting claims, believing that they qualify. And I think in lots of cases, that is what we’ve encountered when we’ve worked with clients, if we’ve inherited from other advisors, and realise that they potentially don’t qualify quite to the degree that they thought they did.

The other side of the coin is the lack of education available within the R&D regime and within this space, because HMRC’s guidance has always been famously quite grey and open to interpretation. It’s an inevitability that there was going to be misunderstanding. I suppose part of our job as advisors is to educate people, sometimes that’s the time of bad news, sometimes it’s time good news.

Quite often though, what we’re trying to do is take them on a journey and ensure that it becomes easier for everyone going forwards. To come to your point about Jeremy Hunt and if what he’s doing is attempting to tackle fraudsters, I think the answer plainly has to be no. He’s just trying to limit damage; all he’s doing is axing the amount of damage that can be done. He isn’t ostensibly increasing scrutiny on the fraudsters, he’s not making penalties for committing fraud more harsh, he’s not making the system easier to administer, he’s not talked about how inquiries are going to change. Rishi previously introduced some changes that are looming. Frankly, it’s damage limitation, it’s a temporary measure before they can really define the future of the scheme.

Matt: 8:22 So the big message is: if your R&D is at stake – it’s quite clear – you’re making good claims, proper R&D, you’re doing R&D, doing innovation, the claims are all valid. There’s nothing to worry about. They will continue for the time being, just at a lower rate of cash coming back.

Joe: 8:48 Yeah, that’s right and I think the important thing to note is that R&D is incredibly generous. And in its current state ahead of these changes, it’s one of the most generous regimes in the world, but it’s also one of the hardest to qualify for. So we need to be mindful that we’re always looking to protect the incentive, but the fundamental purpose of it is to encourage innovation and investment in the UK. And there’s no way that Jeremy Hunt as Chancellor is going to want to disincentivise people to continue to innovate here.

Matt: 9:24 No, because we’re not the only country that does this as well. So we have to remain…

Joe: 9:31 Yeah, there are lots of very big, very established schemes in around the UK that could quite happily house those big players and also these larger SMEs that are really looking to take a hit.

Matt: 9:46 So you touched on it earlier, but back in March this year, Rishi announced some tightening of the R&D claims process, possibly to attack these bogus claims and fraud. So he said, from April next year, there’s three points here, that claims would need affectively to be signed off by a named senior officer of the company. So companies planning to make a claim would have to notify HMRC of their R&D on the day it takes place. So, that stops people claiming going backwards. And the last one was, which was interesting, when companies was asked to provide details of any agent advising them on the claim. I was wondering, is there been any update on those proposals?

Joe: 10:41 Well, there’s something of an update, it’s more of clarity around what each of them is proposing. So say the counter signing of the report by an officer of the company is like you say, it’s no different to the tax return being signed. And frankly, if you’re submitting a claim, without the approval of knowledge of a senior officer, then you’re probably doing something wrong. We don’t see that making an enormous dent in the fraud that’s carried out, other than to say that people recognize their names in a document. For what it’s worth, we’ve been doing that for quite some time, it’s fairly important as part of the compliance process to ensure that you get someone signing it off at that senior level. But it might discourage some of the sort of, I suppose most spurious advisors to use a buzzword that seems to be doing the rounds. The second point remind me was?

Matt: 11:41 Not being able to do prior year claims.

Joe: 11:44 Yes. So actually, there has been an amendment to that, which is to say that if you haven’t claimed or haven’t claimed in the last two years, or have never claimed there is still a bit of an exemption. So, you can look back, you do still have to notify going forward in the year in which you’re going to be carrying out the R&D, your intention to submit a claim. That’s just to stop those massive backwards looking claims, that don’t necessarily have meet the record keeping requirements at HMRC and are quite difficult and time consuming to administer from an inquiry perspective, it will also reduce the outlay to the exchequer quite dramatically.

Matt: 12:22 Has it actually been agreed now? is it in place or…

Joe: 12:26 Well, yeah. They’re coming into play from the first of April.

Matt: 12:32 So that example, how practically would you notify them on that? Has that been announced all?

Joe: 12:38 The details are still to be announced. I mean, I think there might be, it could be a hark back to the online form, which played a brief but bright role in the R&D industry, which went nowhere in the end. But there should be a very simple online process for informing HMRC. Again, it’ll be interesting to see how they administer it…

Matt: 13:02 Yeah definitely.

Joe: 13:05 Final point, details of the R&D tax agent. The purpose of this is to tackle some anonymity that was available to R&D advisors. Largely, those ones that didn’t want to put their name to document or in fact, when submitted document at all, with the tax returns, could do a white paper, just a blank page, send it in, have it signed by or in the name of the company they’re submitting on behalf of and effectively own the contract they have in place with the taxpayer. They’re anonymous, they’re not attached to anything. HMRC don’t like this for obvious reasons. And this just requires agents to put their money where their mouth is, show HMRC the whites in their eyes.

And interestingly, in the US, a tax agent is jointly responsible for the contents of a tax return. It will be very, very interesting to see if that’s where we go with this. It’s certainly lend itself to closer scrutiny to agents themselves and therefore, potential penalties for misrepresentation.

Matt: 14:09 Yeah, no, I see this as simply adding a box to the CT600, which says “who is your agent”, and then they can effectively easily report on it. So they can run a report, which says these are the ones with no agent down and then may increase, and we’ll come onto inquires in a minute…

Joe: 14:30 Of course I mean, it’ll be interesting to see what the contents of those boxes are, because it will have to be name, company number, probably name of a senior officer in order to ensure that people aren’t just popping up different trade names left, right and center, and therefore are able to spread the risk a little bit. We’ve certainly seen that with other tax schemes in the past.

Matt: 14:53 The other point I was going to touch on here is the whole thing we’re finding is, there’s a huge variation in the amount of time it takes for HMRC to issue a repayment on R&D claim at the moment. I mean interestingly, my clients who submit with yourselves don’t seem to have too much of a problem, which is good news.

They just had a very large claim for one of my clients repaid in just over a month, which actually beat my expectations because seeing six to eight weeks is a good timeframe. But there have been other instances where the cash has taken a lot longer to come through from HMRC. Just wondering what your thoughts are on or how are your experiences?

Joe: 15:36 Yeah, I mean, well, firstly, thanks for the plug, I’d love to claim that we have some in-road that gets us express payment terms, but I think it’s largely coincidence. Yes, the delays have been a bit of a bugbear for everyone submitting claims for some time, starting at the beginning of the year, became very apparent in around sort of March that everything was slowing down enormously, and HMRC then actually released a statement that they were tackling and experiencing fraud and abuse within the system. And that’s why every payment was delayed. The payment dates went up to 40 days. But frankly, it was much, much longer than that. And we’re still suffering some of the consequences now, they then sped up over summer.

And in fact, I think in the case that you’re talking about, they were able to really meet their own time timeframes that they set, which they set unrealistically quite some time ago. However, we are now entering a period where through volume of claims at the end of the year, but also presumably the uncovering of some additional fraud and erroneous claims of frequency.

Payments are slowing down again. In a lot of cases, corporation tax payments will be issued automatically through the system, they can be kicked out very quickly. We have in fact seen inquiries into some of those retrospectively after the payments been made. So we need to be mindful, that that does mean that the claim has been processed and approved, there very few are in fact approved for that inquiry. The biggest issue is still with tax credits, which go through series of checks and additional payment checks now for four reasons and various other security purposes. And any sort of backdated losses, any losses that are carried back into prior years, they’re still done quite manually; they take a long time to process. So yeah, lots and lots of frustration with the scheme. And then every now and again, you get an absolute star of a claim that just flies through in no time. Very random, no consistency, I think is probably the buzz on that.

Matt: 17:50 Quite a good time now to move on to inquiries. So quite a hot topic at the moment. I mean, us as a firm, I think we’ve went through several years not even seeing one inquiry come through. I think talking to you, I imagine there’s very few as well. And we were thinking at some point these inquiries have got to start.

Then there was news about maybe 12 months ago that HMRC had started recruiting lots of inspectors, and that something was going to happen. And I think now, there are some coming through. I mean, we haven’t got many in the firm. But there’s a small handful that have started to come through and I’ve had my first experience of claims. I just thought, my experience has been two strands to the claim one is, first of all, HMRC inquiring “is it R&D?” That can be a difficult discussion.

The second, which is a bit easier is like a fraud check. So, they’re effectively saying these are numbers you’ve claimed, send us invoices or whatever to back it up. Is that a similar experience with you or you probably see a lot more than us?

Joe: 19:19 Yeah, well now we do. Yeah, for ourselves. But that’s actually a good thing in so many ways. We have a number of inquiries, some on claims submitted, some on claims that we have or for clients for whom we just represent them on an inquiry basis. You’re right, there seems to be two strands. There’s the R&D inquiry, and then there’s the fraud investigation service inquiry, the two actually mutually exclusive, you can have one, finalize it and then still find yourself victim to the other.

However, it’s very unlikely if you’ve been through an R&D inquiry that HMRC will suspect you’re a fraud, but the other way around is much more regular. What we’re really finding, the fraud investigation service ones are very factual. Having made these payments, they are very clear and apparent, targeting of fraud. And if you can prove those, you can get them closed quite quickly.

The typical agent HMRC R&D inquiries now, whilst they still come in very much a similar format, what we have found is there’s been handing over of the responsibility to these new inspectors. So, you might have got so far down the line with an inquiry that might have been open for a couple of years. And find that right at the last minute gets handed to someone else who goes through the whole process again, I can feel your pain. It’s enormously frustrating, it’s very poorly managed. And quite often you end up going through the same questions over and over.

You rightly touched on the fact that, there were very few inquiries for some time, and that was due to understaffing. And it was also due to HMRC’s and the government’s commitment to supporting businesses through COVID. So we all understand there’s a bit of a mandate to ensure that these claims were processed quickly, that there was as little resistance to what appeared to be qualifying claims. In the first instance, to ensure that UK PLC could continue to function in really difficult and unforeseen circumstances. We’re now paying the price because a lot of the fraud happened in that period, it’s very apparent, and HMRC have a 100 extra people, how up to speed they are and how many of them still here, since they took them on is actually not publicly available. But we are seeing increased scrutiny and we’ve probably seen our inquiry rates increase, maybe twice, there’s maybe doubled in the last year. But that’s still a very acceptable level of inquiry, given the value on offer.

So very slow process in some cases, always frustrating. But it’s a really good opportunity for you to prove your methodology and get a bit of a rubber stamp on the work that you’re doing because, frankly, without an inquiry from time to time, it’s very much opinion based and lots of experience. But it’s nice to get that scrutiny from HMRC. From time to time…

Matt: 22:19 Yeah, I get that. So say we’ve been making claims for a number of years, we’ve got this a bit of a worry but you have to go through R&D and actually HMRC agree that’s R&D. Yeah, that’s quite a relief, isn’t it?

Joe: 22:32 You can look at any other area of tax. You look at VAT CT… VAT inquiries attempt penny, everyone. I mean, everyone gets a VAT inquiry in their life, don’t they? And there’s no reason that R&D shouldn’t be the same. And in fact, if you look at other schemes globally, they’re much more frequent. So, meaning in Canada, you submit your claim and you wait for your inquiry. In America it happens, but they do much the same. Lots of US for R&D advisory firms have a huge team of litigators to deal with inquiries, specifically.

Matt: 23:07 So, the takeaway point there is: we think that inquiries have continued to increase and actually it’s not a bad thing.

Joe: 23:14 They are here to stay and look, when the knowledge within the industry on both client side and advisor side is of a sufficient level that fraud is reduced, errors are reduced. They will be able to loosen the reins, the inquiries will feel less intensive because there’ll be less frequent, there’ll be a higher barrier to entry and a deeper understanding across the industry. So inquiries are here to stay, they may as well intensify for that in the short term, but the future will be protected because of inquiries.

Matt: 23:48 And timescales for resolving an inquiry. Can they vary? What are your experiences?

Joe: 23:55 We’ve had some closed in six weeks, where it’s very clear and apparent R&D. We’ve also had cases where it’s taken upwards of two years. Now in that particular case, we’ve had three different inspectors. They all require the exact same information in various different guises over and over again, we’ve had countless meetings, we then moved on to another inspector and right now actually, we’re just in the death throes, we’re very close to closing it, but quite if we get that done for Christmas, it will be will be quite a celebration, but that’s the worst case scenario. Quite often we’ve seen up to six months. Up to six months is will be considered a satisfactory time frame for an inquiry closure.

Matt: 24:47 Are there any issues that they particularly pick on in inquiries and in the construction industry, which I work with a number of clients on, they picked on the idea of subcontracted… who owns the R&D? Sure, you’re not both claiming you and the subcontractor.

Joe: 25:11 Yeah, for sure. And of course, if the principal contractor is an RDEC company, a large company, they can’t claim for the subcontracting costs. So there’s more potential to lose cash for HMRC, there’s more expenditure required if an SME qualified typically in that instance, certainly that’s a favourite way for them to go. That’s typically about ownership and the structure of the contract. So, things can be cleared up through the contract, and just having the right kind of communications from the outset. Another favourite is subsidies, if subsidized expenditure, you’re working for a client, you’re required to do R&D in order to complete the project, who owns that R&D? It’s effectively subsidized by the by the client, in which case, only internal R&D would ever qualify. So again, that’s much about contract terms, where the expertise lies, autonomy, those kinds of things. Another real favourite, which is interesting, because it doesn’t feature in the current guidelines is record keeping. So record keeping is repeatedly used and we all know that it’s good to have good record keeping for tax purposes, going back six years, it’s the famed number that we’ll stick to. But for R&D purposes, it’s exclusively omitted or exclusively not required, per I think para 13 of the code guidelines. So it’s funny now that they fit features so heavily, it’s not unexpected. But if you don’t have your records, in order, if you can’t prove the time that was spent where of when and the kind of work that certain subcontractors carried out on your behalf, then you’ll find it very difficult to qualify your claims on inquiry. And that’s a bit of a lesson for all of us I think.

Matt: 27:07 Just going to finish now on a question coming in, it’s quite an interesting one. Is there any space in the R&D claim for innovative digital agencies working in AR, augmented reality, and innovative tech for advertising campaigns?

Joe: 27:27 Yeah, it is and I really like that question, because it actually highlights a couple of things. It highlights that R&D can potentially exist in lots of different industries, but also, that innovation in and of itself isn’t necessarily qualifying for R&D purposes. So what I mean by that is you could have a series of technologies that you’re using together that have never been used together in that way. But if they work fairly harmoniously, in order to achieve a certain outcome, the use of lots of innovative technologies that haven’t been used together before, wouldn’t necessarily qualify for R&D.

Now, if you had to integrate those technologies in some way, adapt them, in order for them to work harmoniously, there could be some R&D and the time taken to do that, and the technologies that are developed in order to do that. Additionally, it’s very difficult to know without more detail, actually what they’ve been using, what technologies, were they invented for this purpose, have I fundamentally improve the way that this piece of tech is used, because I’ve managed to make it interact with this technology over here and this one over here and these screens now used to work with those kinds of cameras, but now they do because we were able to circumvent this piece of the technological challenge. And whilst the answer isn’t simple, and typically is yes, it can qualify, it’s very difficult to know without digging deeper into what the innovative technologies are and how they interact with one another.

Simply placing innovative technologies next to one another, doesn’t qualify. Bringing them together and making them work as one could, however… It feels like the big yes and no type answer is a good place to finish.

0

The information in this article was correct at the date it was first published.

However it is of a generic nature and cannot constitute advice. Specific advice should be sought before any action taken.

If you would like to discuss how this applies to you, we would be delighted to talk to you. Please make contact with the author on the details shown below.

Comment on this...

Share

Registration is now open for UK businesses to apply for a share of up to £25million for ‘game-changing and commercially viable R&D Innovation’ in the shape of Innovate UK’s Smart Grants.

Registration is now open for UK businesses to apply for a share of up to £25million for ‘game-changing and commercially viable R&D Innovation’ in the shape of Innovate UK’s Smart Grants. Applicants have until the end of October to demonstrate that their innovations can deliver economic benefits.

They apply to businesses across any sector and come at a time when high energy prices have underlined the need to apply new thinking to our infrastructure and buildings. Grants are available for game-changing, innovative and disruptive ideas that will lead to new products, processes or services. With businesses facing so many new challenges, new thinking needs to be on the agenda in every boardroom.

Don’t miss out

With the 26 October deadline fast approaching, make sure you don’t miss out on valuable resourcing to help your business build a resilient future. Full details on the Smart Grants and how to apply can be found here.

0

The information in this article was correct at the date it was first published.

However it is of a generic nature and cannot constitute advice. Specific advice should be sought before any action taken.

If you would like to discuss how this applies to you, we would be delighted to talk to you. Please make contact with the author on the details shown below.

Comment on this...

Share

Many highly innovative and skilful construction businesses are contributing significantly to the UK economy and having access to HMRC’s R&D relief scheme has enabled them to develop and enhance technologies in their field.

The construction industry is one of the largest sectors making claims under HMRC’s R&D relief schemes. Many highly innovative and skilful construction businesses are contributing significantly to the UK economy and having access to HMRC’s R&D relief scheme has enabled them to develop and enhance technologies in their field.

Matt Cook of Goodman Jones and Joe McGurk of Kene Partners discussed the implications in a webinar and here we distil the key points.

What’s going on with HMRC enquiries into construction R&D claims?

Enquiries can be opened on the basis of randomised spot checks or targeted technical queries. Their figures show between 2-5% of all claims have been enquired into, but actually they are quite confidently stating that they’ve increased their enquiry rate by a hundred percent this year so we can imagine that to now be between 5 and 10%.

That’s still actually quite a low number when you consider some 80,000 claims were submitted last year. Which is a phenomenally large number. And following on from the Research & Development Communication Forum this month, they believe that the same number or slightly more will be submitted again this year.

However, this year we’ve actually seen very few enquiries. Some people in the industry think it’s a little bit of calm before the storm, and that something is coming in conjunction with some of the changes that have been outlined recently.

What does HMRC look for in raising an inquiry into an R&D claim?

There are a number of things they can look at. They can enquire on the basis of whether you are carrying out qualifying activities, incurring qualifying expenditure or it can be understanding of the boundaries of R&D projects – that is when R&D begins and ends in the context of the wider commercial project.

The most important thing is that if you have a robust methodology which supports the expenditure that you’ve identified in your claim and there is demonstrable understanding of the guidelines and legislation, then you’re going to be in a good position to resist any HMRC enquiry. What they are really focusing on at the moment are erroneous claims, fraudulent claims if we want to be a little bit fantastical with the expression.

But largely it’s people who are claiming when they shouldn’t be. And that’s been an enormous issue for HMRC coming off the back of £300 million identified as fraudulent or erroneous claims last year. They’re understandably cautious about issuing out credits without due diligence.

What happens when you get an enquiry into an R&D claim?

It often starts very broadly, but they normally have a focus that’s either financial or technical. You’ll get a letter outlining some of their concerns. The more you communicate with them the more you start to understand actually where the concern is. An enquiry often has to do with boundaries, technical understanding, very rarely to do with the size of the claim when you get down to the nitty gritty. You will be invited to respond with evidence and they may do the same.

Actually, if it qualifies, it qualifies, and they are very good in that respect. This is why we do not encourage tax payers to shy away from making large claims, provided they are accurate. The suggestion that you can ‘fly under the radar’ with a small claim has never been less true than now.

HMRC will outline any further queries and you can either make an agreement or not. And then after that, of course, it can go to appeal.

In theory it is quite a clean process. In practice, it’s very drawn out. It can be quite invasive, and incredibly frustrating.

If we received money from HMRC does that mean they’ve approved the claim and there won’t be an enquiry?

People erroneously think that because they’ve received money that HMRC effectively has approved their methodology, the qualifying status of the work they have carried out and their understanding of the boundaries of R&D, and that’s absolutely not the case.

We have to remember these are self-assessment forms so the majority of them will just be processed as would a normal tax return. It’s only those 10% that go to an enquiry that are really scrutinised. Which is why people can be lulled into thinking everything is in order. Actually HMRC requirements year on year increase as the scheme matures, therefore the scrutiny you pay to the technical and financial elements of your claim should also increase.

How long after the claim can HMRC launch an enquiry?

In practice it’s a year. We’ve seen it stretch a little bit further than that. An agent typically hides behind the concept that they’re protecting taxpayer money and they can take as long as they want to. If there is a suspicion of fraud then the timeline for enquiry can be much longer.

What does the Quinn London case mean for R&D claims in construction?

The Quinn London case, is particularly important for construction clients. It’s the first big one that’s hit the news. HMRC have picked up an enquiry and disagreed with a particular point which is about ‘subsidised R&D’. That is where work is carried out for a client and the R&D expenditure is deemed to have been ‘subsidised’ by the fees paid for that work. HMRC’s argument was that if you’re carrying out work that is contracted to you by a client, and that work requires R&D and you’re paid to do that work, then it is subsidised R&D on the basis that its part of the contract with the client. However, for now HMRC has lost the first-tier tribunal in what is in some respects a landmark case.

That was thrown out because in effect that would mean that people who do work for clients can’t claim R&D which is a simplification of the summary but really is the crux of it. The Quinn London case actually ended up being successful on the basis that HMRC focused on subsidised expenditure and had a really narrow and unfair interpretation of the legislation.

Having spoken with some of the HMRC inspectors, they actually feel like they missed an opportunity to challenge on a subcontractor basis and they’ve made it very clear that their stance remains the same. Just because they’ve lost one doesn’t mean they won’t contend on exactly the same conditions in the future, which is encouraging in some ways, because they are being consistent.

What is concerning about this stance is that some of us were hoping this would offer some level of precedent. They’ve been very clear. The Quinn ruling offers no precedent so we won’t be able to bring it up in future enquiries.

Is there a big risk then for subcontractors making claims being paid from main contractors?

HMRC is obviously narrowing the scope of R&D and it’s a contentious issue. We disagree with HMRC’s stance on sub-contractors R&D and subsidy. There’s a 65% cap already.

Is there anything subcontractors can do currently to protect their position?

The company can really protect itself by preparing to dispel the evidential burden with documentation and evidence and show the role between the sort of time and organisation for whom the work was delivered and the party has given the instruction or with the autonomy for resolving the uncertainties.

It’s really important that contracts are clear about what is included. You can actually go as far as to say, this will not include any subsided costs got for R&D. You could be really explicit in your contract and that would really help. But in lieu of that, the best thing you can do is evidence that you are the experts carrying out R&D independently of the company that has contracted you to do it without their direction.

However, in the construction sector, quite often, the conversations will happen on the phone. So it’s about getting into the habit of documenting the work you’re doing because it will protect you down the line.

The focus on record keeping has become more and more important. People are going to have to be able to keep records and evidence of the work that they’re doing. And it might go as far as needing to make applications for R&D within the year that the R&D is carried out.

What’s the future for R&D tax incentives?

There is some good news and some bad news. The good news is that HMRC have broadened the scope a little bit. So they are going to allow costs for cloud hosting, computing, and data, which they’ve resisted for years and years but are completely valid areas of expenditure.

Some slightly worse news is that they are intending to remove the ability to claim for sub-contracted R&D that’s carried out outside of the UK. That will be extended to EPWs (externally provided workers). They haven’t confirmed whether or not it will affect companies with branches in other countries, but I think we can safely assume that if they’re not subject to PAYE in the UK, they won’t qualify. Beyond that, there’s a lot of focus on automation and fraud reduction, and a move towards a digital submission. It’s all part of the refining of the process, but also addressing some serious fraud that’s been undertaken in the industry.

Budget for R&D incentives going forward

The intention is that it will amount to 2.4% of GDP by 2027/28, which is an astronomical amount of money. £8 billion was claimed last year and that number goes up year on year. HMRC say they are willing and they want to be able to invest that money, that they want to award it to businesses in the UK, but they do have to address the leakage that’s been caused by erroneous claims and misunderstanding of the schemes. Both advisers and taxpayers are equally at fault for the number of fraudulent claims that have been made.

Whilst that’s good news for legitimate claims, in the short term, there will be some real administrative burden. However, the average claim size in the UK for SMEs is about £50,000 pounds so it may not be unreasonable to see a tightening of the rules being required.

How will R&D claims be submitted?

Returns and claims will have to be submitted by the online portal as you would normally submit a tax return. Historically it’s been possible to email them through to an inbox. This encourages, or at least enables a little bit of that kind of misbehaviour from certain agents, whereby they might white label their report so that HMRC doesn’t know who they have been prepared by.

It also takes away the need for the due diligence that is undertaken when a tax return is submitted. Above that, there’s also a suggestion that we will be required to make an application or give notice of intention to submit an R&D claim within a financial year.

Why do we need to give the name of our R&D agent?

It gives HMRC the opportunity to target agents they know who are submitting erroneous claims or don’t have a good understanding of the scheme. It means that you really have to put your name to the claims you’re submitting. This coupled with the digital submission will really address some of the big issues that rogue agents have brought to the industry.

0

The information in this article was correct at the date it was first published.

However it is of a generic nature and cannot constitute advice. Specific advice should be sought before any action taken.

If you would like to discuss how this applies to you, we would be delighted to talk to you. Please make contact with the author on the details shown below.

Comment on this...

Share

The most common question at the moment is what happens where a Group company (ConstructCo Ltd) carries out the construction work and charges to a fellow Group subsidiary company that owns the property (PropCo Ltd).

Who is affected by the changes to the Reverse Charge?

From 1 March 2021, all UK VAT registered individuals or businesses that receive or supply standard or reduced rate services reported within the Construction Industry Scheme need to consider the new domestic VAT reverse charge scheme.

Suppliers

Suppliers must use the reverse charge from 1 March 2021 if they are UK VAT registered and:

– the customer is UK VAT registered.

– payment for the supply is reported within the Construction Industry Scheme (CIS).

– the services are standard or reduced rated.

– they are not an employment business supplying either staff or workers, or both.

– their customer has not given written confirmation that they are an end user or intermediary supplier.

What should a supplier do now?

1. Check their customer has a valid VAT number.

2. Check their customer’s CIS registration.

3. Review their contracts and if the reverse charge will apply, tell their customers.

4. Ask their customer to confirm if they are an end user or intermediary supplier (see below).

5. Work out how to record the reverse charge in their accounts.

If the customer confirms they are an end user, the reverse charge does not apply. Invoices should be raised with no change and VAT applied and accounted for as before.

I am a supplier and have confirmed the reverse charge applies. What do I do from 1 March?

– Sales invoices should be raised with no VAT (although still a taxable supply).

– Ensure the invoices state that the reverse charge applies.

– Report the sales in the Turnover box only on your VAT Returns.

– Customers will no longer pay you the VAT element. This could have a considerable cashflow impact. You should consider moving to monthly VAT returns to aid the cashflow burden.

What do the changes to the Reverse Charge mean for buyers?

Buyers must use the reverse charge from 1 March 2021 if they are UK VAT registered and:

– Payment for the supply is reported within the Construction Industry Scheme (CIS).

– The supply is either standard or reduced rated.

– They are not hiring either staff or workers, or both.

– They are not an end user or intermediary user (see below).

What should a buyer do now?

1. Check their supplier has a valid VAT number.

2. Determine whether or not they are an end user or intermediary user. If they are an end user or intermediary user then they need to inform their supplier.

3. Work out how to record the reverse charge in their accounts.

If the buyer is an end user or intermediary user, then the reverse charge does not apply. Invoices should be received with no change and VAT applied and accounted for as before.

I am a buyer and have confirmed the reverse charge applies. What do I do from 1 March?

– From 1 March 2021, ensure that invoices received from suppliers are correct and if within the reverse charge scheme, are raised with no VAT.

– Record the reverse charge on your VAT return. This means:

o Calculate what the VAT input tax would be and put this is the purchase input tax box.

o Enter the same amount in the output tax box. This cancels with the above so has no overall effect on the VAT being paid/claimed.

o Include the purchases amount (which excludes any VAT) in the purchases box.

Am I an “end user”?

Consumers and final customers are called “end users”. For the purposes of the Construction Industry and the VAT Reverse Charge, this will mean businesses, or groups of businesses, that are UK VAT and CIS registered but do not make onward supplies of the building and construction services provided to them.

In practical terms, for property and construction companies, this will usually be the company that owns or leases the property where the works are taking place.

The reverse charge does not apply to end users (as long as the end user informs their supplier in writing that they are an end user)

What about a Corporate Group scenario?

“Intermediary suppliers” are UK VAT and CIS registered businesses that are connected or linked to end users. To be connected or linked to an end user, intermediary suppliers must either:

– Have a relevant interest in the same land where construction works are taking place, or

– Be part of the same Corporate Group or undertaking.

The reverse charge does not apply to supplies to intermediary suppliers where the intermediary supplier notifies their supplier or building contractor in writing that they are intermediary suppliers. Intermediary suppliers can refer to themselves as end users.

The most common question at the moment is what happens where a Group company (ConstructCo Ltd) carries out the construction work and charges to a fellow Group subsidiary company that owns the property (PropCo Ltd).

In this scenario, ConstructCo is an “intermediary supplier” and Prop Co Ltd is an “end user”.

The reverse charge will not apply on any transactions between ConstructCo Ltd and PropCo Ltd and will also not apply on any transactions between ConstructCo Ltd and third-party subcontractors. In other words, there is no change from existing procedures.

0

The information in this article was correct at the date it was first published.

However it is of a generic nature and cannot constitute advice. Specific advice should be sought before any action taken.

If you would like to discuss how this applies to you, we would be delighted to talk to you. Please make contact with the author on the details shown below.

Comment on this...

Share

Clear and accurate management reports can inform strategic decisions and satisfy lenders' requirements for transparency.

As every property developer knows, development projects have never been a favoured investment among funders – especially mainstream banks.

Investors tend to see property developments as high-risk options, as the asset they’re being asked to lend against doesn’t yet exist. And in the post-recession climate, and the unpredictable times we find ourselves in, they seem more reluctant than ever to finance them.

In this context, the slightest cause for concern can be enough to discourage funders from taking on property risk. Developers must therefore guard against giving them any excuse to say no.

In my experience, less-than-adequate project accounting can be one such excuse.

Robust project accounting allows a development’s stakeholders to monitor the financial health of the work in progress. Without the transparency it brings, any problems with a scheme could go unnoticed until they cause serious financial damage to the project.

That’s why investors will often insist on seeing evidence of good project accounting before deciding whether to fund a development.

Benefits

Effective project accounting drives several important benefits for property developments.

Firstly, it joins the dots between operations and financial control. It connects the quantity surveyors and project managers on the frontline, with the accountants who report on the development’s financial performance.

It also accurately forecasts and monitors cash-flow and profitability over the course of the development. This provides stakeholders with crucial, up-to-date intelligence on the scheme’s financial situation, and helps prevent any unexpected shortfalls from occurring.

Finally, by ensuring smooth financial performance, sound project accounting keeps funding flowing into the development. And it puts developers in a better light when looking to fund future projects.

Best practice

So how can developers go about ensuring their project accounting is up to the mark? I believe a robust process depends on three vital elements:

1. Forecasting

2. Reporting

3. Timelines

Let’s look at each of these aspects in turn.

1. Forecasting

Project accounting can only be as effective as the forecasts it is based on.

The first step is therefore to create a reliable financial forecast for the development, based on a well set-out project appraisal, accurate costings and, importantly, the right level of detail.

Too little forecast data restricts transparency, and risks introducing inaccuracies. Yet too much will be incomprehensible to stakeholders, also harming transparency. And it will take too long to compile.

2. Reporting

With the forecast in place, actual financial performance data needs to be reconciled against it each month. The aim should be to expose any differences, understand their impact, and identify their cause.

As with the forecast, monthly reports must be presented in a way that can be easily understood and interpreted by a wide range of stakeholders. These include site managers, the board, investors, and so on.

The monthly reports should be discussed by the senior management team. It’s their job to act decisively to address any major variations from the forecast as the project progresses.

Between reports, any unforeseen changes must immediately be reported to stakeholders, along with their implications for the project’s financial situation. Such changes might include construction delays, cost increases, disputes or significant currency movements.

3. Timelines

The key to keeping project accounting on track is to lay down – and keep to – strict deadlines for three key milestones:

1. data to be provided by site surveyors and project managers

2. invoices to be received and input into the accounts

3. monthly management reports to be compiled and distributed to stakeholders

Technical support

Project accounting for property developments is a complex exercise. Getting it right will require input from financial experts with deep experience in the technicalities of the property and construction sectors.

Skilled project accountants will produce clear and accurate management reports that can inform strategic decisions, and of course, satisfy lenders’ demands for transparency. They will also know how to make sense of the numbers, and discern what they mean for a project – and for the business behind it.

Please get in touch if you’d like to discuss project accounting for your property developments.

0

The information in this article was correct at the date it was first published.

However it is of a generic nature and cannot constitute advice. Specific advice should be sought before any action taken.

If you would like to discuss how this applies to you, we would be delighted to talk to you. Please make contact with the author on the details shown below.

Comment on this...

Share

What is particularly good to see is the role that British businesses are playing in that and their role in the innovations that are being brought to the sector.

The Future of Construction report published by Raconteur Media in this week’s (Sunday 27 March 2016) Sunday Times, highlighted the forecasts for the global construction sector growth of more than 70% by 2025 and underline what opportunities there are to be had by those businesses operating in and alongside it.

What is particularly good to see is the role that British businesses are playing in that and their role in the innovations that are being brought to the sector. See the article on Ten ways we are changing the way we build. With so many ways that the sector is adapting, many driven by use of new technologies, but not all, there are great opportunities for businesses to improve site efficiencies and processes.

We have seen this with several of our own construction clients and would urge others to remember that their investment in improving processes and developing new solutions for customers could well qualify for an R&D tax credit.

The information in this article was correct at the date it was first published.

However it is of a generic nature and cannot constitute advice. Specific advice should be sought before any action taken.

If you would like to discuss how this applies to you, we would be delighted to talk to you. Please make contact with the author on the details shown below.

Comment on this...

Share

we were all delighted when we saw how quickly HMRC accepted the claims and in certain instances repaid substantial amounts of tax.

Many construction business owners are missing out on valuable tax breaks because they are under the misapprehension that Research & Development (R&D) tax relief only applies to those conducting formal research, such as pharmaceutical companies.

Any construction company undertaking some form of innovation may qualify for R&D relief. This is much more common than is often thought, with construction companies often coming across a problem and developing a new or unique solution to overcome it. If you have an employee who is a problem solver, for example, one would expect to have a claim and the cost of an employee can be considerable.

Is it worth it?

If you are an SME (Small and Medium-sized Enterprise – fewer than 500 employees and either turnover of up to €100m, or gross assets of up to €86m) you benefit from an enhanced rate of R&D relief. A profit-making SME can claim an additional deduction of 130 per cent of the R&D spend.

For year ending 31 March 2016 – the effective tax saving is 26% of R&D spend

There are separate rules for larger companies. They are restricted to claiming an additional deduction of 30 per cent of the R&D spend.

For year ending 31 March 2016 – the effective tax saving is 6% of R&D spend

What if we’re not making a profit?

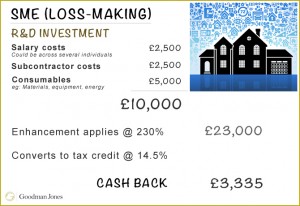

Even loss-making companies may be able to access cash back, which will be particularly welcome by start-ups or those needing cash to fund development.

SMEs can convert 230 per cent of R&D spend into tax credits at a rate of 14.5 per cent and receive cash.

For year ending 31 March 2016 – the effective tax saving is up to 33.35% of R&D spend

For a large company using the R&D Expenditure Credit scheme, a taxable receipt of 11 per cent of the R&D spend is granted.

For year ending 31 March 2016 – the effective tax saving is up to 8.80% of R&D spend

Red tape?

There are time restrictions, so businesses should not delay in finding out whether they might qualify for R&D relief.

Claims must be made within two years of the end of an accounting period but it is possible to go back and amend a tax return to include a claim. So if you submitted a tax return for the year ended 31 December 2014, you have until 31 December 2016 to go back and make a claim.

The claim is a relatively straightforward process, involving explaining what you did in writing and putting the costs against it before the claim figures are included in the computations.

Well worth it

We have guided a number of our clients in the property and construction sector through this and we were all delighted when we saw how quickly HMRC accepted the claims and in certain instances repaid substantial amounts of tax.

0

The information in this article was correct at the date it was first published.

However it is of a generic nature and cannot constitute advice. Specific advice should be sought before any action taken.

If you would like to discuss how this applies to you, we would be delighted to talk to you. Please make contact with the author on the details shown below.

Following David Cameron’s “surprise” announcement at the Conservative annual conference a few days ago, the government have today officially launched Help to Buy Part 2.

Help to Buy Part 2 in simple terms is where a purchaser can buy a property with a just a 5% deposit with the lender purchasing a guarantee from the government covering up to 15% of the value of the property. This reduces the risk to lenders and in theory should increase their willingness to lend to those with smaller deposits at more competitive rates. The scheme is available to both first time buyers and existing home owners buying either a new build or an older property up to the value of £600,000.

I say “surprise” announcement as this all looks quite planned! From today you are able to apply for a mortgage under the scheme from one of the banks currently offering Help to Buy mortgages. Mortgages will only be guaranteed from January 2014, the original launch date advertised. It should be highly unlikely that someone completes in November or December 2013 then defaults before January 2014!

One interesting point to come out of the detail is the fee the government is receiving from the lenders (which effectively will be passed on to the borrowers). The lenders will be charged a fee of up to 0.9% on the total mortgage amount. 0.9% of the £130bn of mortgages expected to be in the scheme is over £1bn for the government – assuming no pay-outs of course! A nice immediate cash windfall!

£12bn of mortgage guarantees has been made available by the government. How popular will the scheme be? Rightmove have announced statistics from their website since Cameron made his announcement that imply huge interest. The doubters are saying this will cause a huge property bubble problem and will be difficult to withdraw. Others are saying availability and the fees charged can be adjusted to keep the scheme under control.

As always, we will wait to see the overall effect on the housing market over the next few years!

0

The information in this article was correct at the date it was first published.

However it is of a generic nature and cannot constitute advice. Specific advice should be sought before any action taken.

If you would like to discuss how this applies to you, we would be delighted to talk to you. Please make contact with the author on the details shown below.

We are delighted to announce that

We are delighted to announce that

Enquiries can be opened on the basis of randomised spot checks or targeted technical queries. Their figures show between 2-5% of all claims have been enquired into, but actually they are quite confidently stating that they’ve increased their enquiry rate by a hundred percent this year so we can imagine that to now be between 5 and 10%.

Enquiries can be opened on the basis of randomised spot checks or targeted technical queries. Their figures show between 2-5% of all claims have been enquired into, but actually they are quite confidently stating that they’ve increased their enquiry rate by a hundred percent this year so we can imagine that to now be between 5 and 10%.