To be successful in X Factor a competitor needs at least three yesses to follow their dreams. In the world of family giving you need to overcome only two hurdles. That doesn’t necessarily mean that family giving is any easier than progressing through the rounds of X Factor.

When one gifts down through the family generations the two taxes which need to be considered are Capital Gains Tax and Inheritance Tax.

Capital Gains Tax

Capital Gains Tax (CGT) is the tax when an individual disposed of an asset, whilst Inheritance Tax can be considered the additional tax on transferring that asset. The Government appreciate that it wouldn’t be right to charge both on a single transaction and therefore there are various reliefs which can be claimed to prevent one of them applying. Ideally there would be no tax on a gift and much succession planning is based around eliminating these taxes.

Gifting Sterling

Capital Gains Tax is only chargeable on certain assets. A commonly gifted asset which has no CGT implication is gifts of Sterling. You will note that I am very specific about the currency. If a gift is made in a currency other than Sterling then there could be Capital Gains Tax considerations.

Gifting Shares

If the gift is of shares in a trading business and the recipient of the gift is a UK tax resident, then there may be the possibility to jointly elect with the donor to holdover or delay the gain element. This effectively means that the donor does not pay any CGT on the gift but the recipient acquires the asset at the same base cost as that applicable to the donor. At best this is a tax deferral as the recipient will pay more tax when they sell the shares.

If the business is not a trading business it may be possible to undertake a demerger to allow a business which would otherwise not qualify for this relief to become qualifying.

Potentially Exempt Transfers

Most gifts of assets are potentially exempt transfers (PETs) for Inheritance Tax (IHT) purposes. In simple terms this means that the gift becomes free of IHT should the donor survive seven years from the date of the gift. To be a PET the gift must be unfettered and there has been talk for many years about the risk of HMRC extending the seven year period to something longer. If the donor dies within the seven year window then not all of the gift falls into IHT. The potential liability tapers away within the seven years and it is possible to buy life assurance which would cover the tax should it become payable within that window.

IHT and CGT

If you pause at that point it would appear that Capital Gains Tax is the primary concern. This is because gifts could potentially be exempt from IHT due to the seven year rule.

Gifts into certain structures can give rise to an immediate IHT charge. In order to prevent both IHT and CGT being payable on the same commercial transaction it is then possible to make a tax election to prevent the CGT being payable. Depending on value and circumstance the IHT may be less than the CGT which would otherwise be payable. This can lead to planning whereby an IHT charge of nil or a modest value is deliberately generated in order to avoid a higher CGT cost. This planning needs to then be tempered with the cost of running the resulting structure or the future cost of unwinding it.

Gifting shares in a trading businesses in a Will

Many trading assets are exempt from IHT. As an alternative to gifting during life and having the recipient take on the donor’s Capital Gains Tax base cost it may be more efficient for the donor to retain the asset and leave it to the recipient in their Will. At death there is no IHT on the trading asset and the asset is transferred to the individual at its market value as at the date of death.

This has led to planning involving business owners and their elderly parents. The business person gifts shares in the family company to their elderly parents and holds over the capital gain. The understanding is that the Will of the elderly parent transfers the asset back to their child. With the right fact pattern the death of the parents does not lead to any Inheritance Tax on the shares and the business person reacquires the shares from the estate of their parent with an uplifted base cost of the assets.

You could say that was a yes, yes and yes.

If you´d like to get future articles to your inbox:

We occasionally write on practical issues within family businesses including succession planning.

The information in this article was correct at the date it was first published.

However it is of a generic nature and cannot constitute advice. Specific advice should be sought before any action taken.

If you would like to discuss how this applies to you, we would be delighted to talk to you. Please make contact with the author on the details shown below.

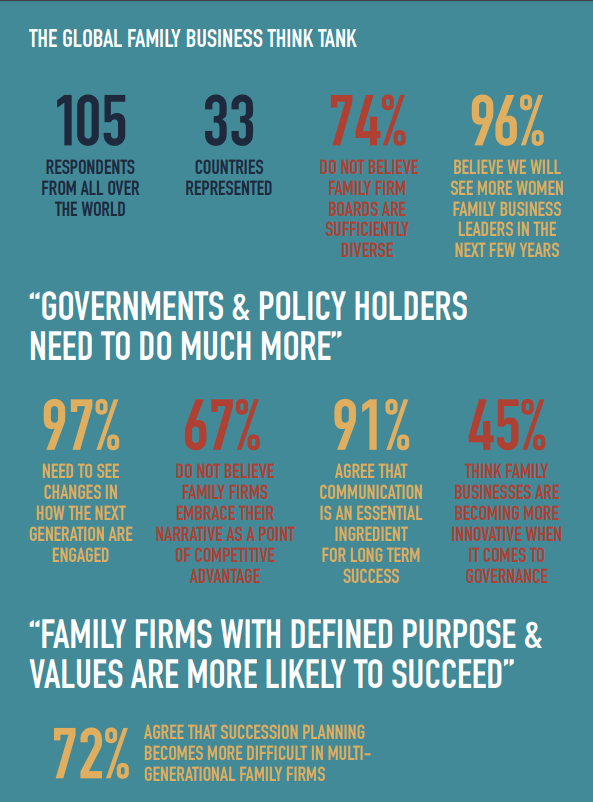

I was delighted to be able to contribute to Family Business United’s inaugural Global Family Business Think Tank.

I was delighted to be able to contribute to Family Business United’s inaugural Global Family Business Think Tank.